If you’ve ever shopped for car insurance, you’ve almost certainly heard the term full coverage car insurance — but here’s a truth most insurers don’t advertise: there is no official policy in the insurance industry actually called “full coverage.” The term is consumer shorthand, a convenient label for a bundle of protections that goes well beyond what your state legally requires you to carry.

At its core, full coverage combines three distinct components: liability coverage, collision coverage, and comprehensive coverage. Together, these three pillars protect you from the financial consequences of accidents, theft, weather events, and lawsuits — risks that minimum-only policies leave dangerously exposed.

The financial stakes are real. A driver carrying only state-minimum liability coverage who causes a serious accident could face tens of thousands of dollars in out-of-pocket costs for vehicle repairs, medical bills, and legal judgments. Full coverage dramatically narrows that exposure — but understanding exactly what you’re buying, and what it won’t cover, is the only way to make a genuinely informed decision.

Your financing status, your state’s laws, the age of your vehicle, and your personal risk tolerance all shape which combination of coverages makes sense for you. This guide walks through every layer — from deductibles and actual cash value payouts to gap insurance and no-fault state requirements — so you can make the right call with confidence.

Key Takeaways

- Full coverage is a colloquial term for a bundle of liability, collision, and comprehensive insurance — not a single official policy type.

- Lenders require collision and comprehensive coverage if you finance or lease your vehicle, protecting their financial interest in the car.

- Liability covers others; collision and comprehensive cover damage to your own vehicle, regardless of fault or cause.

- Choosing a higher deductible lowers your premiums but increases your out-of-pocket costs when you file a claim.

- Actual Cash Value (ACV) payouts account for depreciation and can leave a significant financial gap after a total loss.

- Optional add-ons like gap insurance, roadside assistance, and rental reimbursement fill critical coverage gaps in standard policies.

- State laws dictate minimum liability limits that vary significantly, and no-fault states impose entirely different coverage frameworks.

What “Full Coverage” Actually Means

Full coverage car insurance is not a standardized policy type — it is an informal term consumers and agents use to describe a combination of liability, collision, and comprehensive coverage that provides protection beyond a state’s legal minimum requirements. No insurer issues a policy with “full coverage” printed on the declarations page; instead, you’re buying a customized bundle of individual coverages.

The term emerged as a practical shorthand in the consumer market. When loan officers, dealerships, and agents needed a quick way to distinguish bare-minimum liability policies from more robust protection, “full coverage” filled that gap in the conversation. The phrase implies — correctly — that you’re covered for a wider range of financial risks than the law requires.

It’s worth being precise about what “full” actually means here. Even the most comprehensive bundle of coverages has exclusions, limits, and deductibles. No policy pays for every conceivable loss. Knowing what’s inside the bundle — and what’s missing — is the foundation of smart insurance shopping.

The Three Pillars of Full Coverage

Every full coverage policy is built on three core components, each covering a distinct category of financial risk:

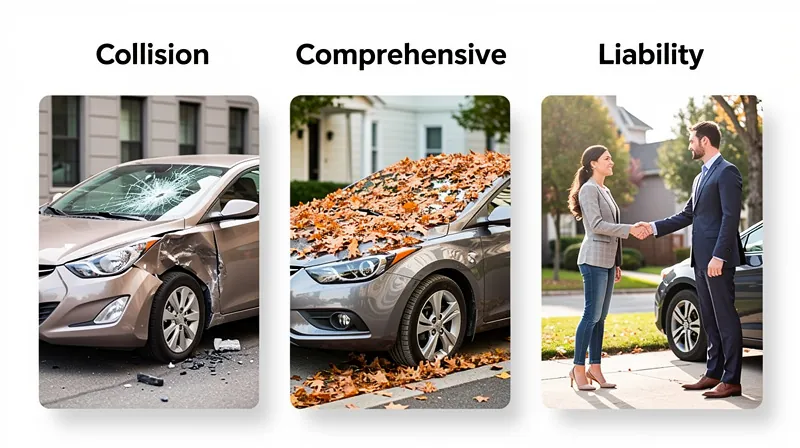

- Liability Coverage: Pays for bodily injury and property damage you cause to other people in an accident. This is the only coverage most states legally require, and it does nothing to repair your own vehicle.

- Collision Coverage: Pays to repair or replace your vehicle when it’s damaged in a collision — with another car, an object, or even a single-car rollover — regardless of who is at fault.

- Comprehensive Coverage: Covers damage to your vehicle from non-collision events, including theft, fire, vandalism, flooding, hail, falling objects, and animal strikes.

Understanding this distinction matters enormously: liability protects your wallet from claims made against you; collision and comprehensive protect your vehicle itself. Drivers who carry only liability are one bad hailstorm or theft away from a total, uncompensated loss of their vehicle.

Coverage Limits and Split Limits

Liability coverage is sold in structured tiers, typically expressed as split limits. A common example is 100/300/50, which means:

- $100,000 per person for bodily injury

- $300,000 per accident for bodily injury (total)

- $50,000 per accident for property damage

Many states require minimums as low as 25/50/25 or even lower — limits that can be exhausted in a single serious accident involving a newer vehicle or significant medical bills. Purchasing limits significantly higher than your state minimum is one of the most important financial decisions you can make.

For collision and comprehensive claims, the payout is typically based on your vehicle’s Actual Cash Value (ACV) — what the car was worth on the open market at the time of the loss, not what you paid for it or what it would cost to replace it today. Depreciation is the key variable here, and it has major financial consequences that many policyholders don’t discover until they file a claim.

Why Lenders Require Full Coverage

When you finance or lease a vehicle, the lender or leasing company holds a financial interest in that car — which means they require collision and comprehensive coverage to protect their asset, not just yours. If your car is totaled and you only carry liability, the lender still expects to be repaid in full, regardless of your loss.

This isn’t optional. Your loan or lease contract will explicitly require you to maintain full coverage for the duration of the financing period. If you drop coverage or let it lapse, your lender has the contractual right to place force-placed insurance on your vehicle — a policy that protects the lender only, at a dramatically higher premium, charged directly to your loan balance.

Once you own your vehicle outright, the requirement disappears — but the financial wisdom of maintaining coverage often remains, depending on your vehicle’s value and your financial cushion.

The Role of Gap Insurance

Gap insurance covers the difference between your vehicle’s Actual Cash Value at the time of a total loss and the remaining balance on your auto loan. This gap can be substantial, particularly in the first two to three years of a loan when depreciation is steepest.

Consider a concrete example: you purchase a new car for $38,000 and finance the entire amount. Eighteen months later, the car is totaled. Your insurer calculates the ACV at $29,000 — but you still owe $34,000 on your loan. Without gap insurance, you owe your lender $5,000 out of pocket for a car you no longer have.

Gap insurance eliminates that $5,000 exposure. It’s particularly critical for buyers who:

- Made a small or no down payment

- Financed over a long term (60, 72, or 84 months)

- Purchased a vehicle with a high depreciation rate

- Rolled negative equity from a previous loan into the new one

Gap insurance becomes unnecessary once your loan balance falls below your vehicle’s ACV — typically around the three-year mark for most vehicles. At that point, you can safely drop it and reduce your premium.

Leasing vs. Financing Requirements

Leasing companies generally impose stricter coverage requirements than traditional lenders. While a bank might simply require collision and comprehensive with reasonable deductibles, a leasing agreement often specifies:

- Minimum liability limits (often 100/300/100 or higher)

- Maximum deductibles for collision and comprehensive (commonly $500)

- Gap coverage as a built-in requirement or optional add-on

Some leasing contracts also allow — or require — paying insurance premiums upfront as part of the lease agreement. Always read your lease contract carefully before purchasing a standalone policy, since falling short of its specific requirements can put you in breach of the agreement even if your policy is technically “full coverage.”

The Financial Mechanics: Deductibles and Limits

A deductible is the amount you pay out of pocket before your insurance coverage kicks in on a collision or comprehensive claim. Your deductible choice is one of the most direct levers you have over your monthly premium — and over your financial exposure in the event of a loss.

The relationship is straightforward: a higher deductible means a lower premium; a lower deductible means a higher premium. What varies is the risk you’re absorbing. Choosing a $1,000 deductible instead of $500 might save you $15–$30 per month, but it means you’ll pay an extra $500 out of pocket every time you file a claim.

Coverage limits, particularly on the liability side, control the maximum amount your insurer will pay in a covered loss. Anything above your limit becomes your personal financial responsibility — which, in a serious accident, could mean wage garnishment, asset liens, or bankruptcy.

Choosing the Right Deductible

The classic deductible decision is between $500 and $1,000. Here’s a practical framework for deciding:

- Choose $500 if: You don’t have a reliable emergency fund, you live in an area with high accident or weather risk, or you’d struggle to cover $1,000 suddenly.

- Choose $1,000 if: You have $1,000 or more in accessible savings, you’re a low-risk driver with a clean history, or the monthly premium savings are significant enough to recoup the difference within 12–18 months.

A simple test: divide the annual premium savings by the deductible difference. If your $1,000 deductible saves you $300 per year over the $500 option, you’d break even in about 20 months — meaning the higher deductible pays off if you go roughly two years without a claim. The higher your risk tolerance and emergency reserves, the more sense a higher deductible makes.

Asset Protection Strategies

Your liability limits are not just about satisfying legal requirements — they are your primary defense against personal financial ruin in a catastrophic accident. A serious multi-car collision or a pedestrian injury lawsuit can generate liability claims in the hundreds of thousands of dollars.

Consider these asset protection principles:

- High-net-worth individuals should carry liability limits of at least 250/500/100 — and strongly consider an umbrella policy that extends coverage to $1 million or more.

- High-risk drivers (young drivers, those with recent violations) paradoxically need higher limits because they’re more likely to be in a serious accident where limits are tested.

- Physical damage coverage (collision and comprehensive) protects your vehicle, not your assets. Don’t confuse the two — they serve entirely different financial purposes.

The general rule: your liability limits should, at minimum, equal the total value of the personal assets a plaintiff could realistically pursue.

Optional Add-Ons That Fill the Gaps

Even a robust full coverage policy has gaps — specific situations where you’d be left paying out of pocket without additional endorsements. Several optional add-ons are worth serious consideration for most drivers, depending on their circumstances.

Uninsured/Underinsured Motorist (UM/UIM) Coverage is among the most critical. Roughly 1 in 8 drivers on American roads carries no insurance at all, according to the Insurance Research Council — and many more carry only bare-minimum limits. If one of these drivers hits you, UM/UIM coverage pays what their insurance can’t. Some states mandate it; in others, it’s optional but essential.

Personal Injury Protection (PIP) and Medical Payments (MedPay) coverage pay for your own medical expenses after an accident, regardless of fault. PIP is broader — it can also cover lost wages and rehabilitation — while MedPay is narrower, covering only medical bills. Both provide faster, more direct access to funds than waiting for a liability claim to resolve.

Roadside Assistance and Towing

Standard roadside assistance packages through an insurer typically cover:

- Towing to a nearby repair facility

- Battery jump-starts

- Flat tire changes (using your spare)

- Lockout service

- Fuel delivery for empty tanks

Insurance-based roadside assistance is usually cheaper than a standalone AAA membership — often $5–$15 per vehicle per year added to your premium — but it may be more limited in scope. AAA and similar standalone plans often provide broader towing distances and additional member benefits. If you don’t have an AAA membership and your insurer offers roadside assistance for a nominal fee, adding it is almost always worth the cost.

Rental Reimbursement Coverage

Rental reimbursement coverage pays for a temporary rental vehicle while your car is being repaired after a covered claim. Without it, you’re paying out of pocket — which can run $30–$60 per day for a basic rental and quickly add up during a lengthy body shop repair.

Typical policy limits range from $30–$50 per day for up to 30 days. Daily commuters and anyone without a second vehicle to fall back on will benefit most from this add-on. The annual premium addition is usually modest — $20 to $40 per year — making the cost-benefit calculation easy for most households.

ACV vs. Replacement Cost: The Depreciation Trap

Actual Cash Value (ACV) is the most common payout method for collision and comprehensive claims, and it means your insurer pays what your car was worth at the time of the loss — after depreciation — not what it would cost to replace it with something comparable today. This distinction can mean a difference of thousands of dollars.

Replacement Cost coverage, by contrast, pays what it actually costs to replace your vehicle with a new one of the same make and model — depreciation removed from the equation. It’s less common in personal auto insurance than in homeowners insurance, but some insurers offer it as an endorsement, particularly for newer vehicles.

The Depreciation Trap

Here’s where policyholders consistently get blindsided. A new car loses approximately 20% of its value in the first year and nearly 50% within three years, according to automotive valuation data. That depreciation is fully reflected in an ACV payout.

A concrete example: You bought a vehicle for $42,000 three years ago. It’s totaled today. Your insurer’s ACV calculation — based on mileage, condition, local market comparables, and depreciation — comes in at $24,000. You walk away with $24,000 minus your deductible, even though replacing the same vehicle with a comparable three-year-old model might cost $27,000–$29,000 in the current market.

Factors that reduce ACV include:

- High mileage relative to the vehicle’s age

- Pre-existing damage or deferred maintenance noted in inspection

- Market conditions (in a soft used-car market, ACV drops further)

- Vehicle depreciation rate (some brands hold value far better than others)

The trap is that most drivers assume their insurance will make them whole — that “full coverage” means full replacement. It doesn’t, unless you’ve specifically purchased replacement cost protection.

When to Choose Replacement Cost

Replacement cost endorsements add to your premium, but for certain vehicles and circumstances, the extra cost is well justified. You should seriously consider this coverage if:

- Your vehicle is three years old or newer, when depreciation is steepest and the gap between ACV and replacement is largest

- You purchased a high-depreciation vehicle (luxury SUVs, some domestic models)

- You’re financing and want to ensure a total-loss payout covers your remaining loan balance

As your vehicle ages past five or six years, the premium cost of replacement cost coverage tends to exceed the practical benefit — at that point, the gap between ACV and replacement shrinks as depreciation slows. Evaluate annually whether the endorsement still pencils out.

When to Drop Full Coverage: A Value Analysis

Dropping collision and comprehensive coverage on an older, lower-value vehicle can make financial sense — but only when you’ve run the specific numbers for your situation, not based on a general rule of thumb. The decision requires honest math, not guesswork.

The commonly cited “10% rule” suggests dropping collision and comprehensive when your combined annual premium for those coverages exceeds 10% of your vehicle’s current market value. For example: if your car is worth $6,000 and you’re paying $800 per year for collision and comprehensive, you’re paying 13% of the vehicle’s value annually for coverage that — after your deductible — might net you only $5,000 in a total-loss claim. That math is hard to justify.

The Break-Even Point

A more precise analysis calculates the net maximum claim value — your vehicle’s ACV minus your deductible — and compares it to your annual premium for those coverages:

- Find your vehicle’s current ACV (use Kelley Blue Book, Edmunds, or NADA guides)

- Subtract your deductible from the ACV (that’s your net payout in a total-loss scenario)

- Compare that figure to your annual collision and comprehensive premium

- If the premium exceeds roughly 10–15% of the net payout per year, the math favors dropping coverage

Important caveat: even if the math says drop it, consider whether you could absorb the full vehicle loss without serious financial hardship. If losing that $6,000 car with no payout would genuinely strain your finances, maintaining coverage — even when it’s not the optimal economic choice — provides real peace of mind and financial stability.

Factors to Consider Before Cancelling

Before dropping collision or comprehensive coverage, honestly evaluate each of these factors:

- Driving history: If you have recent at-fault accidents or live in a high-traffic urban area, your actual probability of filing a claim is higher than average. Don’t drop coverage right before it’s most likely to pay out.

- Location risk: Comprehensive coverage addresses theft and weather. If you live in a hail-prone region, a high-vehicle-theft ZIP code, or an area prone to flooding, comprehensive is earning its keep even for older vehicles.

- Vehicle reliability: An older vehicle that’s also unreliable is a double financial risk. If it’s likely to break down and also at risk of collision damage, the combined exposure is higher than either factor alone suggests.

- Out-of-pocket repair capacity: The real question is whether you can afford to repair or replace the vehicle entirely from savings if it’s damaged or stolen. If the honest answer is no, keep the coverage.

State Requirements and No-Fault Nuances

Every state mandates a minimum level of auto insurance coverage, but those minimums vary dramatically — and the underlying legal framework (tort vs. no-fault) fundamentally changes what “full coverage” needs to include in your state. Buying coverage without understanding your state’s framework is like insuring against the wrong risks.

In the majority of states — tort states — the driver who causes an accident is financially responsible for all resulting damages. This is the traditional system: liability coverage pays victims of the at-fault driver’s negligence. In contrast, no-fault states require each driver’s own insurance to pay for their medical expenses, regardless of who caused the accident, with restrictions on suing the at-fault party.

Navigating No-Fault States

Twelve states currently operate under a no-fault insurance framework, including Florida, Michigan, New York, New Jersey, and Pennsylvania. In these states:

- Personal Injury Protection (PIP) is mandatory, not optional, and covers medical expenses, lost wages, and related costs for the policyholder regardless of fault

- The right to sue the at-fault driver for pain and suffering is restricted to cases meeting a specific “serious injury” threshold (which varies by state)

- PIP coverage requirements vary widely: Michigan’s no-fault system is among the most expansive in the country, while other states have minimal PIP thresholds

In no-fault states, full coverage necessarily includes robust PIP coverage. Skimping on PIP limits in a no-fault state is a particularly costly mistake, since your own insurer — not the at-fault driver’s — is your primary source of medical cost recovery.

State-Specific Add-Ons

Beyond the no-fault vs. tort distinction, states vary considerably in other coverage requirements:

- Uninsured Motorist (UM) coverage is mandatory in approximately 22 states and the District of Columbia. In states where it’s optional, the high rate of uninsured drivers makes it a near-essential purchase.

- Medical Payments (MedPay) is required in Maine and New Hampshire and is a common add-on elsewhere. It functions similarly to PIP but typically without the lost-wage component.

- Premium costs are also heavily location-dependent. Drivers in Michigan, Florida, and Louisiana consistently pay among the highest rates in the country due to litigation environments, weather risk, and uninsured driver rates. Wyoming and Vermont drivers typically pay far less.

Always verify your state’s specific minimum requirements before purchasing or modifying a policy. State insurance department websites are the most reliable source for current, accurate minimum coverage data.

Frequently Asked Questions

What does full coverage mean with car insurance?

Full coverage car insurance is an informal term for a combination of liability, collision, and comprehensive insurance coverage. It is not an official policy type but rather a consumer term describing protection that goes beyond state-minimum liability requirements. Together, these three coverages protect you from financial losses caused by accidents you cause (liability), accidents involving your vehicle (collision), and non-collision events like theft or weather (comprehensive).

Who is the cheapest full coverage auto insurance?

The cheapest full coverage auto insurance varies by driver profile, location, and vehicle, so there is no single provider that is cheapest for everyone. Nationally, insurers like GEICO, State Farm, and USAA (for military members) consistently rank among the most competitive on price, but rates are highly individualized based on your driving record, age, ZIP code, and credit history. The most reliable way to find the lowest rate is to compare personalized car insurance quotes from at least three to five insurers annually.

How much does a $1,000,000 liability insurance policy cost?

A $1,000,000 liability limit through a personal umbrella policy typically costs between $150 and $300 per year, making it one of the most cost-effective forms of financial protection available. Auto liability limits on a standard car insurance policy rarely reach $1 million on their own; instead, drivers achieve that level of protection by combining standard auto liability limits with an umbrella policy that activates after the underlying policy’s limits are exhausted. The exact cost depends on your driving record, the number of vehicles covered, and the insurer.

How much is insurance for a Nissan Xterra?

Full coverage insurance for a Nissan Xterra typically costs between $1,200 and $1,800 per year, though the exact figure depends heavily on the driver’s age, location, driving history, and selected coverage levels. The Xterra’s discontinuation after the 2015 model year means most insured examples are older vehicles, which often qualify for lower collision and comprehensive premiums due to reduced ACV. Getting personalized car insurance quotes from multiple insurers is the best way to find an accurate rate for your specific Xterra and circumstances.

Is full coverage mandatory in all states?

No — full coverage car insurance is not legally required in any state. Every state mandates some form of liability insurance (or an equivalent financial responsibility requirement), but collision and comprehensive coverage are never legally required for vehicle registration. They become effectively required when you finance or lease a vehicle, because your lender or leasing company contractually mandates them to protect their asset. Once your loan is paid off, the decision to maintain full coverage is entirely your own.

What is the difference between liability and full coverage?

Liability coverage pays for damage and injuries you cause to others, while full coverage also includes protection for your own vehicle through collision and comprehensive insurance. A liability-only policy is the minimum legal requirement in most states and will not pay a cent toward repairing or replacing your vehicle after an accident or theft. Full coverage adds collision and comprehensive to that base, giving you financial protection on both sides of an accident — for others and for yourself.

What is gap insurance and do I need it?

Gap insurance covers the difference between what your car insurance pays out (the vehicle’s Actual Cash Value) and what you still owe on your auto loan after a total loss. You need it most acutely in the first two to three years of financing a new vehicle, when depreciation is steepest and your loan balance is most likely to exceed the car’s market value. If you made a substantial down payment, are near the end of your loan term, or own your vehicle outright, gap insurance is generally unnecessary.

Does full coverage cover a rental car?

Full coverage car insurance typically extends your collision and comprehensive protections to a rental car, but rental reimbursement coverage — which pays for the cost of the rental itself — is a separate, optional add-on. Your standard collision and comprehensive coverages will generally protect a rented vehicle from physical damage in the same way they protect your own car, which means you can often decline the rental company’s costly collision damage waiver. However, if your car is in the shop after a covered claim and you need a rental, you’ll only receive reimbursement for that rental’s cost if you specifically purchased rental reimbursement coverage on your policy.