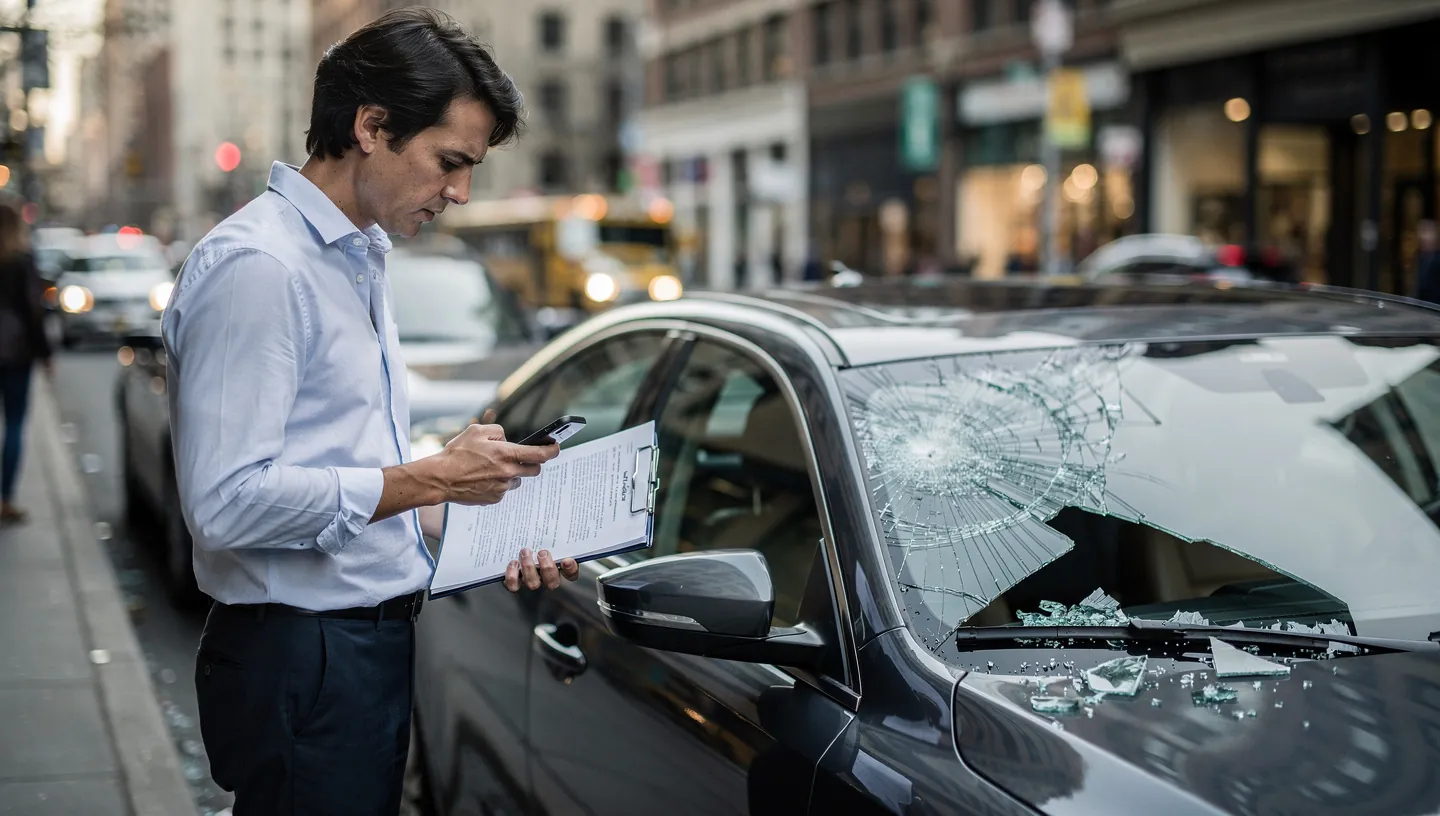

A broken car window can happen in an instant — a stray rock on the highway, a hailstorm in the parking lot, or a smash-and-grab theft outside a grocery store. When it does, the first question most drivers ask is: does auto insurance cover broken car windows? The short answer is yes, but only under the right circumstances and with the right coverage in place.

Coverage depends entirely on how the damage occurred. Comprehensive coverage, collision coverage, and liability insurance each play distinct roles based on the cause of the break. Understanding which policy applies — and how your deductible affects your out-of-pocket cost — is the difference between a stress-free claim and an unexpected bill.

This guide covers every scenario: from a simple chip repair to a full windshield replacement on a vehicle equipped with advanced driver assistance systems (ADAS). You’ll also learn whether filing a glass claim will raise your premiums, when to pay out-of-pocket, and what to do if you don’t have comprehensive coverage at all.

Key Takeaways:

- Comprehensive coverage pays for broken windows caused by non-collision events like rocks, hail, and vandalism.

- Collision coverage applies when the break occurs during a crash with another vehicle or object.

- Liability insurance from an at-fault driver may cover your window if someone else hits your car.

- Most insurers waive deductibles for windshield repairs, but not always for full replacements.

- Filing a glass-only claim rarely increases your premiums — the risk is far lower than most drivers assume.

- Modern windshields equipped with ADAS sensors can cost $1,500 or more to replace, making coverage critical.

Which Coverage Applies to Your Broken Window?

The auto insurance coverage that pays for a broken car window depends on the cause of the damage. Comprehensive coverage handles non-collision events — rocks, hail, vandalism, and theft. Collision coverage activates during crashes, and the at-fault driver’s liability insurance applies when someone else is responsible. Identifying the correct coverage upfront saves time and protects your claims history.

Coverage applies across all glass surfaces — windshields, side windows, and rear glass — though terms may vary by insurer. Some policies prioritize windshield glass due to its structural role, while others apply identical deductible rules to all glass claims. Always review your declarations page to confirm your policy’s specific glass provisions before a loss occurs.

Comprehensive Coverage: The Non-Collision Hero

Comprehensive coverage is the most commonly used policy for broken car windows. It protects against damage that occurs outside of a collision with another vehicle or object. Qualifying events include:

- Flying rocks or road debris striking your windshield

- Hailstorms cracking or shattering glass

- Falling branches or trees

- Animal strikes (such as a deer jumping into your windshield)

- Vandalism, including intentional glass damage

- Theft-related smash-and-grab break-ins

Comprehensive coverage applies equally to side windows and rear glass, not just the windshield. If your car window was broken during a break-in — a common scenario in urban areas — this is the coverage you’ll file under. The critical requirement: you must carry comprehensive coverage. It is not included in a basic liability-only policy.

Collision Coverage: The Crash Defender

Collision coverage activates when your vehicle sustains damage from a physical impact — hitting another car, striking a guardrail, or colliding with a stationary object such as a pole or parking barrier. If your windshield shatters from the force of a crash, collision coverage pays for it.

One important limitation: collision coverage does not cover damage caused by a third party who is at fault for hitting your vehicle. In that scenario, you pursue the other driver’s liability insurance first. Only if their coverage is insufficient — or they are uninsured — would you fall back on your own collision coverage.

Liability Insurance: The At-Fault Driver’s Role

If another driver hits your parked or moving vehicle and breaks your window, their liability insurance is responsible for the repair — not your own policy. This is the core purpose of liability coverage: compensating others for property damage caused by the insured driver.

Always pursue the at-fault driver’s insurer first. Filing under your own policy when someone else is responsible can affect your claims history unnecessarily. If the at-fault driver is unidentified — such as in a hit-and-run — or is uninsured, your own uninsured motorist property damage (UMPD) coverage may apply, depending on your state and policy terms.

Deductibles and Out-of-Pocket Costs

Your deductible is the amount you pay out-of-pocket before insurance coverage begins. For glass claims, standard deductibles typically range from $100 to $1,000, and the relationship between repair cost and deductible determines whether filing a claim is financially worthwhile.

Many insurers treat windshield repairs differently from full replacements, and a growing number of states have enacted laws that shift the equation in consumers’ favor. Understanding these distinctions before you file — or decline to file — can save you money.

Understanding Your Deductible

Here is how the deductible mechanic works in practice: if your comprehensive deductible is $500 and a rock chip repair costs $150, your insurer pays nothing — you cover the full $150 because the damage doesn’t exceed your deductible. If a full windshield replacement costs $900, your insurer pays $400 ($900 minus your $500 deductible) and you cover the remainder.

Drivers with high deductibles to lower monthly premiums often find themselves paying entirely out-of-pocket for all but the most significant glass damage. A lower deductible raises monthly premiums but makes smaller claims financially viable to file. Use this framework when evaluating your options:

- Repair costs ($50–$150) rarely exceed a standard deductible — pay out-of-pocket

- Basic replacement costs ($300–$600) may or may not exceed your deductible — compare carefully

- ADAS-equipped windshield replacements ($800–$1,500+) almost always make filing a claim worthwhile

Full Glass Coverage Endorsements

Full glass coverage is an optional endorsement — also called a glass deductible waiver — that eliminates or significantly reduces your deductible for auto glass claims. It is one of the most cost-effective add-ons in auto insurance, typically costing $2 to $5 per month.

For that modest cost, you gain the ability to file windshield repair and replacement claims with zero or minimal out-of-pocket expense. This endorsement delivers the greatest value for drivers who regularly travel highways where road debris is common, those in hail-prone regions, and anyone driving a newer ADAS-equipped vehicle where replacement costs are high. Some insurers now bundle “weather glass” packages that combine full glass coverage with roadside assistance and rental reimbursement under a single monthly add-on — worth asking about at renewal.

Repair vs. Replacement: Making the Right Choice

Not every broken or chipped window requires a full replacement. A professional repair is often structurally sound, faster, and significantly cheaper — and insurers actively prefer repairs because they cost less to pay out. The decision depends on the size, location, and depth of the damage.

Choosing incorrectly carries consequences beyond cost. A windshield that needed replacement but received only a repair can compromise your vehicle’s structural integrity — windshields account for up to 30% of a car’s structural rigidity in a rollover. A professional assessment before deciding is always the right move.

When Is a Repair Sufficient?

A chip or crack is generally repairable when all of the following conditions apply:

- The crack is smaller than 6 inches in length

- The chip is no larger than a quarter

- The damage does not extend to the edge of the windshield

- The damage is not in the driver’s primary line of sight

- The inner layer of the glass is undamaged

Repairs typically cost between $50 and $150 and can be completed in under an hour. Many insurers waive the deductible entirely for small chip repairs — it is simply cheaper to pay $100 for a repair now than $1,000 for a replacement later. If your insurer offers a deductible waiver for repairs, use it. A small chip left unaddressed can become a full crack overnight in cold weather.

The Cost of Replacement and ADAS Calibration

Full windshield replacement costs more than most drivers anticipate — especially in newer vehicles. Basic replacement on an older standard vehicle runs $300 to $600. On luxury vehicles, electric vehicles, or any modern car with ADAS, the cost climbs to $1,000 to $1,500 or more.

The primary driver of that higher cost is ADAS calibration. Modern windshields house cameras, radar sensors, and other components that power lane departure warnings, automatic emergency braking, and adaptive cruise control. When the windshield is replaced, these systems must be precisely recalibrated to factory specifications before they function correctly. Skipping this step is not just a warranty issue — it is a safety hazard.

ADAS recalibration adds an estimated $200 to $400 to any replacement job, and some high-end vehicles require dealer-level calibration that pushes total costs past $2,000. Key points every driver should know:

- Calibration must be performed by a certified technician using specialized equipment

- Not all auto glass shops are equipped for ADAS calibration — verify capability before scheduling

- Full glass coverage endorsements increasingly include calibration within their coverage scope

- Inform your insurer that calibration is required when filing — it changes the total claim amount

OEM (original equipment manufacturer) glass is a related cost factor worth discussing with your insurer. Some policies specify OEM glass only; others permit aftermarket alternatives. OEM glass ensures the precise fit and sensor compatibility the manufacturer intended but costs more. If you drive a newer or premium vehicle, confirm your policy’s glass specification language before a loss occurs.

What If You Don’t Have Comprehensive Coverage?

Without comprehensive coverage, you have no insurance protection for broken windows caused by non-collision events. This is a significant and frequently underappreciated financial gap. A hailstorm, a rock chip, a parking lot break-in — every one of these scenarios leaves you fully responsible for the repair or replacement bill if comprehensive coverage is absent from your policy.

This situation affects more drivers than many realize. Industry estimates suggest roughly one in eight drivers carries only liability insurance. If you are among them, understanding your exposure and your options is essential to making informed decisions about both your vehicle and your coverage.

Scenarios Where You Are Fully Liable

Without comprehensive or collision coverage, the full financial burden of a broken window falls on you in these common situations:

- A rock flies off a truck and shatters your windshield — no comprehensive means no coverage

- A hailstorm cracks multiple windows while your car sits in a parking lot

- Vandals break your side window overnight — comprehensive would cover this; liability does not

- You back into a pole and crack your rear window — without collision coverage, you pay out-of-pocket

- A deer strikes your car and breaks your windshield — classified as a comprehensive event, not collision

The cost exposure is real. A single hailstorm can generate $500 to $2,000 or more in glass damage across multiple windows. For a driver carrying only liability insurance, that entire bill is out-of-pocket. Comprehensive coverage typically costs only $100 to $300 annually for most vehicles — a modest premium relative to the risk it eliminates.

Pursuing the At-Fault Driver

If a third party caused the damage — another driver who hit your parked car, or a neighbor whose actions damaged your vehicle — you have legal recourse even without your own comprehensive coverage. Start by documenting everything: photograph the damage, gather witness information, and obtain the other party’s insurance and contact details.

In many cases, the at-fault driver may prefer to pay you directly rather than file a claim with their own insurer and risk a premium increase. Send a formal written invoice for the repair or replacement cost, including any ADAS calibration fees. If they decline, you have two options:

- File a claim directly with their liability insurer — you do not need your own insurer to facilitate this process

- Pursue the matter in small claims court if the amount falls within your state’s limit, typically $5,000 to $10,000

If the driver is uninsured or fled the scene without leaving information, your options are limited without your own uninsured motorist property damage (UMPD) coverage. This is a compelling reason to carry more than the state-required minimum liability policy.

Impact of Claims on Your Insurance Premiums

One of the most persistent misconceptions in auto insurance is that filing any claim — including a glass claim — will automatically trigger a premium increase. For glass-only claims, this belief is largely a myth. The reality is more nuanced, and understanding it helps you make smarter filing decisions without unnecessary hesitation.

Premium increases are typically tied to at-fault accidents and driver negligence — events that signal future risk to the insurer. A rock striking your windshield on the highway reflects nothing about your driving behavior. That distinction is central to how most insurers classify and price glass claims.

Myth-Busting: Do Glass Claims Raise Rates?

Glass-only claims have a very low probability of raising your premiums. In many cases, fewer than 10% of glass claimants see any rate adjustment following a single claim. Several factors explain why:

- Glass damage is typically classified as an “act of nature” — an uncontrollable event, not a driver error

- Insurers that do adjust rates for glass claims typically apply a minimal surcharge ($20–$40 annually) that disappears after one claim-free year

- Many states have regulations that specifically limit rate increases for comprehensive glass claims

- Multi-policy discounts — such as bundling home and auto — can offset any marginal increase entirely

For context, an at-fault collision claim can raise premiums by 20% to 40% for three to five years. The risk profile of a glass claim is categorically different. Treating both with the same level of caution is rarely warranted and may lead to missed savings.

When to File vs. Pay Out-of-Pocket

Despite the low premium risk, there are still situations where paying out-of-pocket is the more practical choice. Use this framework to guide your decision:

- File a claim if the damage cost is close to or exceeds your deductible, especially for ADAS-equipped replacements

- File a claim if you have full glass coverage with a waived deductible — there is virtually no reason not to

- File a claim if the damage is extensive and involves multiple windows or structural concerns

- Pay out-of-pocket if the repair cost ($50–$100) is well below your deductible and the damage is minor

- Pay out-of-pocket if you have filed multiple claims in the past 12 months and are concerned about policy non-renewal

The key variable is always your deductible. A $100 deductible against a $400 repair makes filing the clear financial choice. A $1,000 deductible against a $200 repair means you pay the full amount regardless — filing serves no financial purpose.

2026 Trends: Full Glass Coverage and ADAS

The auto glass insurance landscape is changing rapidly, driven by two converging forces: legislative expansion of glass coverage protections and the widespread integration of ADAS technology into new vehicles. Drivers purchasing or renewing policies in 2026 should understand these developments — they directly affect both available coverage options and out-of-pocket costs.

The opportunity is real: more states and insurers are offering better glass coverage terms than ever before. The risk is equally real: failing to update your policy to reflect what’s available means leaving meaningful protection on the table.

The Rise of Zero-Deductible Policies

A growing legislative trend is pushing insurers in certain states to offer zero-deductible glass coverage options — and in some cases, mandating it outright. As of 2026, approximately 18 states have laws or insurer-adopted policies that either waive glass deductibles or require insurers to offer the waiver as an option to policyholders.

Florida has historically led on glass coverage protections, giving drivers the right to file a windshield claim with no deductible under comprehensive coverage. South Carolina, Massachusetts, and Kentucky are among the states expanding similar consumer protections. The broader industry trend points toward “weather glass” package bundling, where insurers combine zero-deductible glass coverage with other weather-related protections under a single endorsement — improving both accessibility and value.

If you live in a state with these protections and your insurer has not informed you, ask directly. Many drivers are entitled to zero-deductible glass coverage and are simply unaware.

Modern Windshields and Sensor Calibration

The integration of ADAS technology into windshields is the single biggest shift affecting auto glass insurance today. In 2020, fewer than 30% of new vehicles had windshield-mounted camera systems. By 2026, that figure exceeds 70% of new vehicle sales — meaning the majority of cars on the road in the coming decade will require sensor recalibration after any windshield replacement.

This shift carries three major implications for policyholders:

- Claim amounts are higher: Insurers must now account for calibration costs in every ADAS-related glass claim, pushing average replacement payouts significantly upward

- Full glass endorsements are more valuable: Policies that waive deductibles now increasingly include calibration in their scope, representing hundreds of dollars in additional protection per claim

- EV-specific considerations matter: Electric vehicles such as the Tesla Model 3 and Ford Mustang Mach-E use specialized acoustic glass and have unique sensor configurations, making replacements more expensive and requiring certified EV glass technicians

The bottom line for modern drivers: auto glass is no longer a simple commodity repair. It is a high-tech, safety-critical vehicle component. Insurance coverage that keeps pace with this reality — specifically full glass coverage that includes ADAS calibration — is not an optional luxury. It is a sound financial protection against a genuine and growing risk.

Frequently Asked Questions

Is it worth claiming a broken car window on insurance?

Yes, in most cases — particularly when repair or replacement costs approach or exceed your deductible. For ADAS-equipped windshields where replacement can exceed $1,500, filing a claim is almost always the right financial decision. For minor chips that cost less than your deductible to fix, paying out-of-pocket is typically more practical. Importantly, glass claims rarely raise premiums, which further supports filing whenever the numbers justify it.

Will my insurance go up if I claim a broken windshield?

It is unlikely. Industry data indicates fewer than 10% of glass claimants see any premium increase following a single glass-only claim. Most insurers classify windshield damage as an “act of nature” rather than driver negligence, which carries little to no underwriting penalty. If a surcharge does apply, it is typically minimal and short-lived — far less impactful than an at-fault collision claim.

Who pays for a broken car window?

Payment responsibility depends on the cause and the coverage available. Your comprehensive insurer pays for non-collision damage — rocks, hail, vandalism — minus your deductible. If another driver is at fault, their liability insurance pays. If you lack the relevant coverage and no other liable party exists, you pay out-of-pocket.

What window is not covered by insurance?

Insurance does not cover glass damage from normal wear and tear, manufacturing defects, or pre-existing damage that was not reported when the policy was written. Drivers carrying only liability insurance have no coverage for any window damage under their own policy, regardless of cause. Coverage gaps most often stem from excluded perils or the absence of comprehensive coverage entirely.

Does full glass coverage cost extra?

Yes. Full glass coverage is an optional endorsement that typically costs $2 to $5 per month, added to your comprehensive premium. It waives your deductible for windshield repairs and, in many cases, replacements — including ADAS calibration costs. For most drivers, a single windshield replacement claim more than offsets years of endorsement premiums.

Can I get roadside assistance for a broken window?

Roadside assistance does not typically cover glass repair or replacement. It is designed for breakdowns, flat tires, lockouts, and fuel delivery. Some premium roadside or auto club memberships include emergency glass services as a specific add-on, but for standard glass coverage, your comprehensive policy or full glass endorsement is the correct coverage to use.

Does comprehensive insurance cover cracked side windows?

Yes. Comprehensive coverage applies to all vehicle glass — including cracked or broken side windows — provided the damage resulted from a covered non-collision event such as vandalism, theft, hail, or road debris. The same deductible rules that apply to windshield claims generally apply to side window claims. Verify your policy’s specific glass language to confirm equal treatment across all glass surfaces.

What does ADAS calibration mean for my windshield?

ADAS calibration is the process of precisely realigning the cameras, sensors, and radar components embedded in or near your windshield after a replacement, restoring the full functionality of safety features including automatic emergency braking, lane-keeping assist, and adaptive cruise control. Calibration is a mandatory safety step that typically costs $200 to $400, must be performed by a certified technician, and should be disclosed to your insurer when filing a replacement claim since it increases the total claim amount.

What if I don’t have comprehensive coverage?

Without comprehensive coverage, you are personally responsible for all glass damage caused by non-collision events — hail, vandalism, rock chips, and break-ins. Your options are to pay out-of-pocket, pursue the at-fault party directly if one exists, or file a claim with the at-fault driver’s liability insurer. Adding comprehensive coverage typically costs $100 to $300 per year and is strongly recommended for any vehicle with meaningful market value.

How much does it cost to replace a windshield?

Windshield replacement costs range from approximately $300 to $600 for older or standard vehicles, and $800 to $1,500 or more for newer vehicles with ADAS technology. Luxury and electric vehicles can exceed $2,000 when OEM glass and mandatory calibration are factored in. This wide cost range makes it especially important to know your deductible before deciding whether to file a claim or pay out-of-pocket.

Should I fix a rock chip myself or use insurance?

Using insurance is almost always the better option if your insurer waives the deductible for chip repairs — as many do. DIY repair kits cost $10 to $30 but risk trapping air bubbles, weakening the repair, and potentially flagging prior damage that could complicate a future insurance claim. A professional repair costs you nothing when covered and produces a structurally sound result. Reserve DIY approaches only for the smallest cosmetic scratches on non-structural glass.

Does hitting a deer cover my broken window?

Yes. A deer strike is classified as a comprehensive claim, not a collision, because it involves an animal rather than an impact with another vehicle or stationary object. Comprehensive coverage pays for all resulting glass damage, including windshield and side windows, subject to your deductible. This classification is financially favorable for most drivers, since comprehensive deductibles are typically lower than collision deductibles.